Editor’s Brief

A practical guide to the "2026 workflow" for opening Hong Kong bank accounts entirely via mobile apps. By leveraging an "information gap" regarding digital documentation—specifically the same-day Entry/Exit record—users can bypass traditional branch queues to secure multiple accounts (HSBC, ZA, Ant, Airstar) within an hour, though legacy systems like Bank of China HK remain prone to technical failure.

Key Takeaways

- The "Golden Ticket" Document:** Success hinges on downloading a PDF of your "Entry/Exit Record" from the National Immigration Administration's WeChat mini-program on the actual day of application. Banks like HSBC reject records generated even one day prior.

- Physical Presence is Non-Negotiable:** While the process is digital, apps use GPS and NFC to verify you are physically within Hong Kong borders. Attempting this via VPN or from the mainland will result in an immediate flag.

- The HSBC "Initialization" Trap:** Completing the 33-step in-app application is not the end. Users must set up their security questions and mobile banking credentials while still in Hong Kong; failing to do so often renders the account inaccessible once you cross back to the mainland.

- Virtual Banks as the Path of Least Resistance:** ZA Bank, Ant Bank, and Airstar offer the lowest friction, often approving accounts in minutes. These serve as excellent backups if traditional Tier-1 banks like BOC fail due to app glitches or strict photo requirements.

- Long-term "Account Maintenance":** To avoid "dormant" status or sudden closure, accounts must show activity (small transfers or QR payments) every six months. Large, immediate transfers back to mainland accounts are a primary trigger for anti-money laundering (AML) freezes.

Introduction

The following content is compiled by VIPSTAR in combination with X/social media public content and is for reading and research reference only.

focus

- I went to Hong Kong and opened four bank cards. The whole trip took less than an hour. No need to go to the counter, no queues, just use the hotel WiFi + mobile app and you’re done.

- No matter how complicated it is said on the Internet, it is actually just an information gap – if you know it, it is very simple, but if you don’t know it, you will hit a wall everywhere. I referred to several guides on Xiaohongshu, plus my own…

Remark

For parts involving rules, benefits or judgments, please refer to Lu Liqing_JimmyLv 2𐃏26’s original expression and the latest official information.

Editorial comments

This article “X Import: Lu Liqing_JimmyLv 2𐃏26 – 2026 latest version to open a card in Hong Kong, get four bank cards in one hour – only Bank of China overturned” comes from the X social platform, the author is Lu Liqing_JimmyLv 2𐃏26. Judging from the completeness of the content, the density of key information given in the original text is relatively high, especially in the core conclusions and action suggestions, which are highly implementable. I went to Hong Kong and opened four bank cards. The whole trip took less than an hour. No need to go to the counter, no queues, just use the hotel WiFi + mobile app and you’re done. Only Bank of China Hong Kong failed. 😂 No matter how complicated it is said on the Internet, it is actually just an information gap – if you know it, it is very simple, if you don’t know it, you will hit a wall everywhere. I compiled this tutorial by referring to several guides on Xiaohongshu and adding in my own pitfalls. Why apply for a Hong Kong Card? Four words: open up the pipeline. Hong Kong dollar/US dollar account, the assets are not all deposited in one basket. Open a Hong Kong and US stock account… For readers, its most direct value is not “knowing a new point of view”, but being able to quickly see the conditions, boundaries and potential costs behind the point of view. If this content is broken down into verifiable judgments, it would at least include the following aspects: I went to Hong Kong and opened four bank cards, and the whole journey took less than an hour. No need to go to the counter, no queues, just use the hotel WiFi + mobile app and you’re done. ; No matter how complicated it is said on the Internet, it is actually just an information gap – if you know it, it is very simple, but if you don’t know it, you will hit a wall everywhere. I referred to several guides on Xiaohongshu and added my own… Among these judgments, the conclusion part is often the easiest to disseminate, but what really determines the practicality is whether the premise assumptions are established, whether the sample is sufficient, and whether the time window matches. We recommend that readers, when quoting this type of information, give priority to checking the data source, release time and whether there are differences in platform environments, to avoid mistaking “scenario-based experience” for “universal rules.” From an industry impact perspective, this type of content usually has a short-term guiding effect on product strategy, operational rhythm, and resource investment, especially in topics such as AI, development tools, growth, and commercialization. From an editorial perspective, we pay more attention to “whether it can withstand subsequent fact testing”: first, whether the results can be reproduced, second, whether the method can be transferred, and third, whether the cost is affordable. The source is x.com, and readers are advised to use it as one of the inputs for decision-making, not the only basis. Finally, I would like to give a practical suggestion: If you are ready to take action based on this, you can first conduct a small-scale verification, and then gradually expand investment based on feedback; if the original article involves revenue, policy, compliance or platform rules, please refer to the latest official announcement and retain the rollback plan. The significance of reprinting is to improve the efficiency of information circulation, but the real value of content is formed in secondary judgment and localization practice. Based on this principle, the editorial comments accompanying this article will continue to emphasize verifiability, boundary awareness, and risk control to help you turn “visible information” into “implementable cognition.”

I went to Hong Kong and opened four bank cards. The whole trip took less than an hour. No need to go to the counter, no queues, just use the hotel WiFi + mobile app and you’re done.

Only Bank of China Hong Kong failed. 😂

No matter how complicated it is said on the Internet, it is actually just an information gap – if you know it, it is very simple, but if you don’t know it, you will hit a wall everywhere. I compiled this tutorial by referring to several guides on Xiaohongshu and adding in my own pitfalls.

Why apply for a Hong Kong Card?

Four words: open up the pipeline.

- HKD/USD account, assets are not all deposited in one basket

- Hong Kong and US stock account opening, overseas SaaS payment collection, overseas consumption payment

- Bank of China Hong Kong ← → Bank of China Mainland mutual transfer with the same name has zero handling fee

- Bind the WeChat Hong Kong wallet, and you can scan the QR code to spend directly when you return to the mainland (it does not count against the foreign exchange settlement quota)

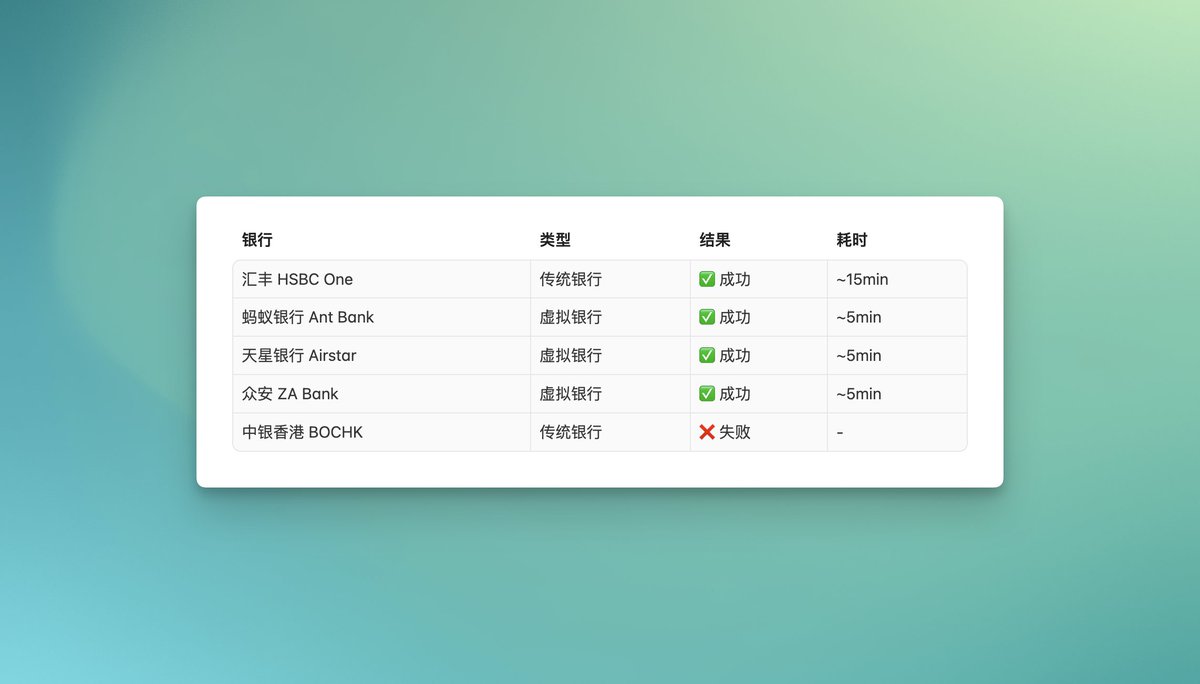

Record: 4 successes, 1 overturn + 1 domestic result

🇭🇰 Open an account online the same day you arrive in Hong Kong

There is no need to go to the bank counter during the whole process of opening a card in Hong Kong! All operations were completed on the mobile app, and four cards were processed in less than an hour.

Preparation before departure (the step that determines success or failure)

📱 Necessary materials

- Hong Kong and Macau Pass (validity period ≥ 6 months)

- Mainland ID card

- Entry and Exit Record PDF ⬅️ Many people don’t know this

- Mobile phone (HSBC requires NFC function, and activating roaming in advance requires receiving text messages)

📋 How to obtain the PDF of entry and exit records?

Few people mention this, but it is a must-have material for opening an HSBC account:

- Search “National Immigration Administration” mini program on WeChat

- Click “Entry and Entry Record Inquiry”

- Download PDF Save to mobile phone

🚨 Personal test and pitfalls: PDF must be from the same day!

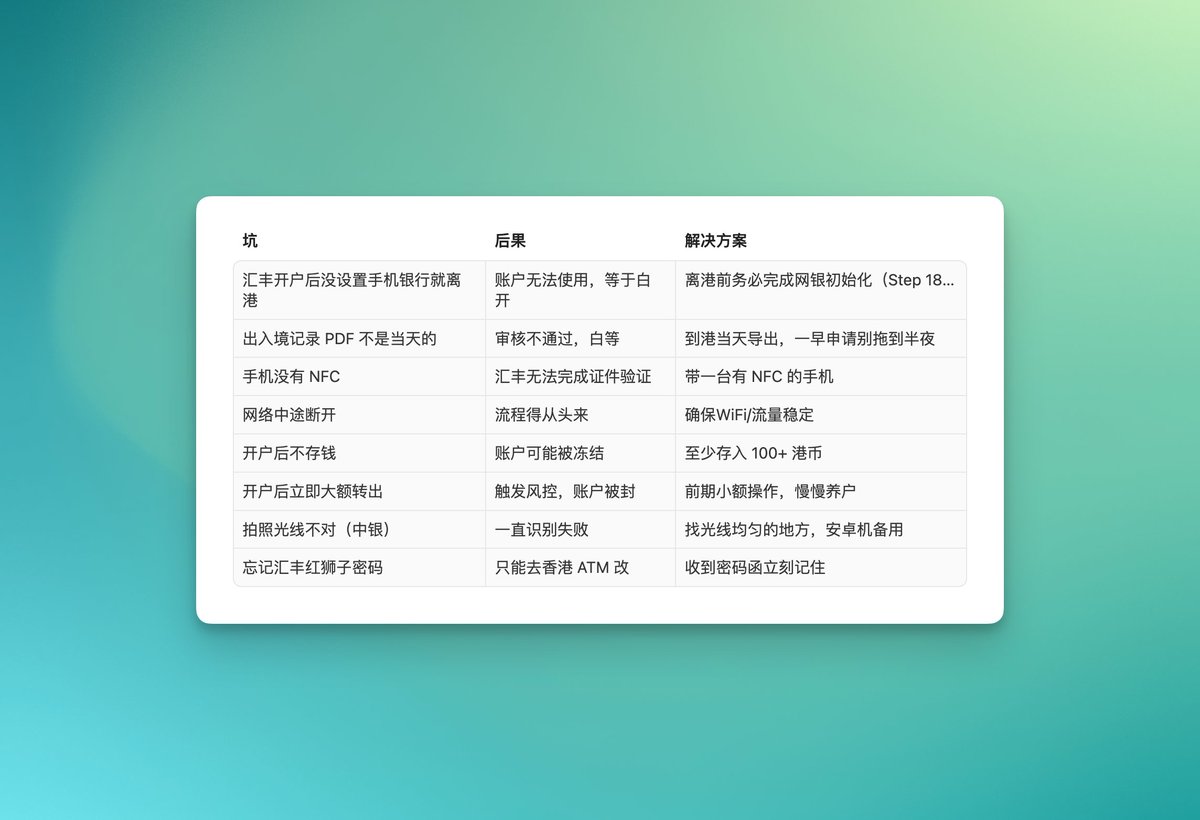

Both HSBC and BOC require that the export date of the immigration record PDF is the same day. I started applying at around 11 o’clock in the evening, but when the bank reviewed it, it was already past midnight and became “the next day”. The system saw that the PDF date was “yesterday” and it failed to pass the review directly.

Suggestion: Option 1: Start applying early in the morning (8 or 9 a.m.), and the application will be approved on the same day.

Option 2: Wait until midnight, re-export the PDF of today’s date, and then apply together. It will only be valid if you export it on the same day you arrive in Hong Kong.

📲 Download apps in advance

Pack it up in the mainland before departure! When you arrive in Hong Kong, drive directly to:

- HSBC HK (App Store / Official Website APK)

- ZA Bank

- Ant Bank Ant Bank

- Airstar Bank

- Bank of China Hong Kong BOCHK (Although I didn’t succeed, you can try)

💡 Android users may need to download the APK from the official website for some apps, which may not be available in domestic app stores.

🌐 Network preparation

- Activate international roaming: Contact the operator before departure to activate the Hong Kong and Macau data package

- Hotel WiFi is also OK: I just used the hotel WiFi and there was no problem throughout the process.

- Key: Ensure network stability! Some people’s WiFi disconnected while they were on, and they had to start from the beginning again.

📝 Other preparations

- Prepare a Mainland Bank Class 1 Debit Card Number (required to open a Zhongan account)

- Proof of address for mainland address (credit card bill/utility bill, backup)

- Think about the purpose of opening an account: “Personal asset allocation” and “overseas consumption” are enough.

Practical procedures for opening accounts in various banks

🏦 1. HSBC One (most recommended, about 15 minutes)

Background: One of the largest banks in Hong Kong, global account linkage, cross-border remittances arrive instantly. The Mainland Industrial Bank Universal Life Card can realize zero-cost remittances to HSBC (Industrial Bank waives handling fees + telecommunications fees, and HSBC charges no intermediary bank fees and deposit fees).

Operation steps (33 steps in total, don’t miss the last step!):

- Open the HSBC HK App → Click “I don’t have any account”

- Confirm “In Hong Kong” → Select “No Hong Kong ID Card”

- Choose to apply for an “HSBC One” account

- Select “Investment Savings” for the reason for opening an account → Select “Online Application” for the application method

- Enter your usual email address → select +86 as your mobile phone area code and receive the verification code

- Select “China” for nationality → select “Pass to and from Hong Kong and Macau” for document type

- Turn on mobile phone positioning and make sure it shows that you are currently in Hong Kong

- Click “Verify Identity Now” → Take a clear picture of the front and back of the pass and upload it

- Follow the prompts to complete face recognition (find a place with sufficient light)

- Verify the filled-in information word by word → turn on the NFC sensor and read the pass information

- Upload entry and exit record PDF

- Fill in your place of birth, occupation, and company name (fill in the truth)

- Select “Personal” for the account type → Select all sources of funds recommended

- Fill in the card receiving address in Pinyin, write it concisely in two lines, and note the mainland mobile phone number at the end.

- It is recommended that the monthly income be less than 50,000 (more than 50,000 requires additional proof of income)

- For tax status, select “Is a Chinese tax resident” → fill in your Mainland ID number for tax number

- Agree to the terms → Submit application

Two results:

- ✅ “Account opened successfully” → Do Step 18 now!

- ⏳ “Further review” → Wait for the physical card (red lion) + password letter to be sent to activate

🚨 Lessons learned in blood and tears! Step 18: Must be completed before departure, otherwise it will be in vain! ! !

Many people submit their applications and leave Hong Kong thinking they are done, only to find out that it doesn’t work! Mobile banking initialization must be completed before leaving Hong Kong: set a unique username (be sure to remember it)

Set an online banking login password (it’s a bit more complicated, so keep a record)

Set 3 security questions + answers (for password retrieval, don’t forget them)

Log in to online banking to complete all initialization operations

Only after completing this step can you truly open an account successfully! Missing this step = total failure!

Other notes:

- ⚠️ People must be in Hong Kong! GPS positioning detection, if you are not in the port area, the app will not allow you to continue.

- ⚠️ Starting from January 2026, HSBC One’s new regulations: Those with total assets of less than HK$10,000 will need to pay a monthly management fee of HK$100

- ⚠️ The Red Lion Card (UnionPay) password can only be changed at HSBC/Hang Seng ATMs in Hong Kong. Remember the initial password!

- ✅ Blue Lion Card (MasterCard) needs to be actively applied for in the App, and it will also be mailed by EMS

- ⚠️ Don’t even open an account on Hong Kong’s public WiFi! The signal is unstable and it is easy to get stuck. Use hotel WiFi or buy a phone card.

🏦 2. ZA Bank (fastest, about 5 minutes)

Background: ZhongAn Online (jointly launched by Ant Group + Tencent + Ping An of China) is a virtual bank, ranking first in Hong Kong, with deposits exceeding HK$16.8 billion and 800,000+ users. There are many exchange rate promotions.

Operation steps:

- Open the ZA Bank App after arriving in Hong Kong

- Register with mobile phone number

- Upload ID card + Hong Kong and Macau pass

- face recognition

- Fill in personal information (mainland bank card number required)

- Submit → usually passes quickly

Things to note:

- The physical card will not be sent automatically, you need to apply for it in the App (payment)

- There is no physical card and it does not affect the use.

- There are many exchange rate coupon activities, and the exchange rate is very cost-effective.

🏦 3. Ant Bank / Airstar (virtual bank)

Ant Bank: A wholly-owned subsidiary of Ant Group (the parent company of Alipay), opening in 2020.

Tianxing Bank: Xiaomi Group (approximately 50.3%) + Futu Holdings (approximately 44.11%) + AMTD Group (approximately 5.6%). Futu may further increase its holdings and become the controlling shareholder in 2025.

The process is similar to Zhongan, basic operations:

- Download App → Register mobile phone number

- Upload documents (ID card + pass)

- face recognition

- Fill in personal information

- Submit for approval

Virtual bank approval can be as fast as a few minutes or as slow as one working day. It is recommended to apply on the first day you arrive in Hong Kong so that you can use it on the same day or the next day.

🏦 4. BOCHK BOCHK (I failed 😂)

Background: Hong Kong branch of Bank of China. The biggest advantage is that there is zero handling fee for domestic transfers between BOC and BOCHK with the same name (through “BOC Express”). In addition, the Mainland Industrial Bank World Life Card can also be transferred to BOC Hong Kong. The Industrial Bank charges no handling fee. However, BOC Hong Kong may charge a deposit fee of approximately HK$60 (above HK$500), so BOC Express is truly zero-cost.

Why recommended but I didn’t succeed:

BOCHK is the most friendly to mainlanders, but there are some pitfalls when opening an account online:

Common reasons for failure:

- The app has extremely strict lighting requirements for taking photos, and even a little reflection/blurring is not enough.

- WiFi is disconnected in the middle → the whole process has to be restarted

- For iPhone users (especially iPhone 16), ID card recognition is easily out of focus.

- Mainland visitors can only open an account through investment and financial management, and need to provide financial management certificates

If you want to try BOCHK, we recommend:

- 📱 Bring an Android device as a backup (higher recognition success rate)

- 🌐 Make sure the network is stable and uninterrupted throughout the process

- 📄 Prepare relevant certificates for investment and financial management in advance (screenshots of fund holdings, stock transaction records, etc.)

- 💰 Select “Free Financial Management” as the account type (10,000 threshold but no compulsory deposit when opening an account)

🏦 5. China Merchants Bank Hong Kong Branch Hong Kong Card (open an account in China, no need to go to Hong Kong)

Background: Note that “Hong Kong All-in-one Card” is a product of China Merchants Bank Hong Kong Branch (bank code 238), not CMB Wing Lung Bank. Although both belong to the China Merchants Bank Group, they are two completely different banks with different account systems, bank codes, and SWIFT codes. China Merchants Bank Hong Kong Branch: CMB’s branch in Hong Kong has only one office and its product is “Hong Kong All-in-One Card”

CMB Wing Lung Bank: an independent legal entity, formerly Wing Lung Bank in 1933, with 35+ branches in Hong Kong

I used to apply for this card through China Merchants Bank to witness the account opening when I was working in China. There is no need to go to Hong Kong.

But to be honest, the threshold is already very high now – it is said that you need to be a private banking client of China Merchants Bank or have average daily assets of more than 5 million to apply. In the early years, the threshold was much lower, so I was able to catch up.

Key operations after opening an account (if you don’t do it, you may open it in vain)

✅ Things to do immediately

- Transfer small amounts of funds: deposit at least HKD 100 to prevent account freezing

- Set up online banking/mobile banking: Make sure the App login is normal

- Bind commonly used functions: FPS, Apple Pay, etc.

- Record account information: take screenshots to save account numbers, online banking usernames, etc.

⚠️ Things to note when raising households (extremely important!)

Many people open their cards and leave them alone. As a result, their accounts are frozen/closed:

- Stay active: make at least one small transfer or purchase every six months

- Don’t transfer large amounts in the early stage: especially don’t transfer back to a mainland card immediately after opening an account! This is the main reason for being banned

- Transfer under the same name: The transferred funds must be transferred between accounts under your own name.

- Avoid frequent large-amount transactions: It is recommended that no more than 3 large-amount transfers be made per month

- Compliant use: Do not participate in any gray transactions, banks have strict anti-money laundering reviews

📬 Physical card mailing

- HSBC: Red Lion (UnionPay) will be sent by EMS, Blue Lion (MasterCard) will be sent by EMS after applying through the App

- BOCHK: surface mail! It’s very slow. It’s normal to wait a few weeks. It’s recommended to add your mobile phone number at the end of the address.

- Virtual Bank: No physical card by default, apply in the App if necessary

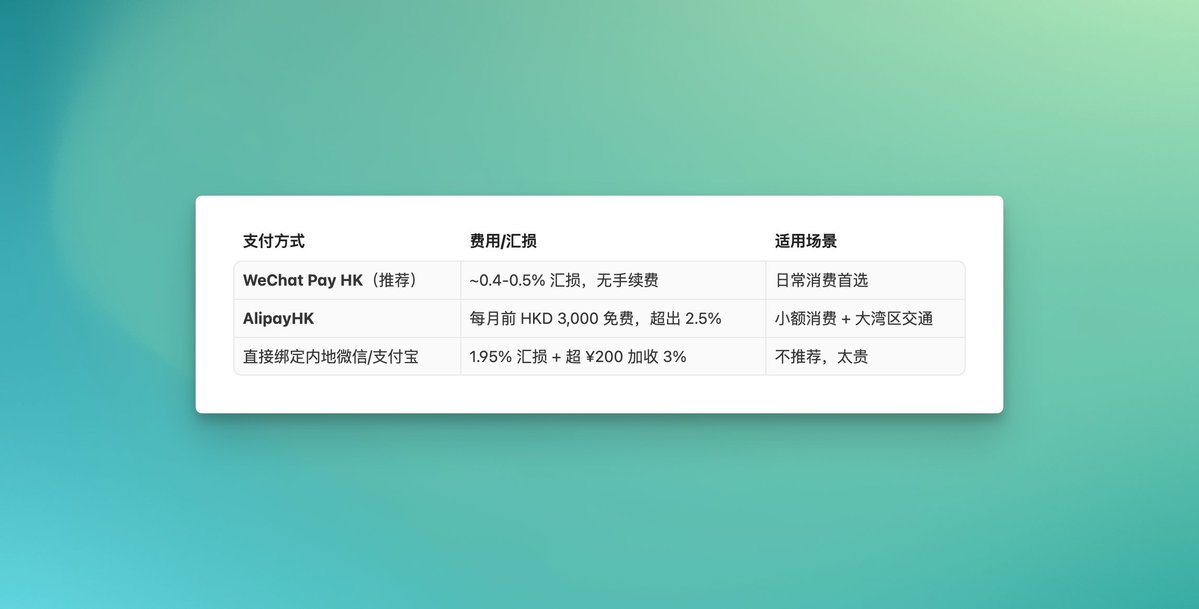

Bind your Hong Kong card to WeChat/Alipay and swipe it directly when you return to the mainland

The most exciting thing about opening a Hong Kong card: After binding the WeChat Hong Kong wallet, you can scan the QR code and make purchases in the mainland as usual. The key is not to take up the annual personal foreign exchange quota of US$50,000 – isn’t this better than currency exchange?

Recommended solution: WeChat Pay HK (WeChat Hong Kong Wallet)

This is the lowest fee plan, with exchange rate losses of only about 0.4%-0.5% and no additional handling fees.

Activation steps:

- Search “WeChat Pay HK Good Life” mini program on WeChat

- Select “Self-Service Opening of Hong Kong Wallet”

- Register with your Mainland ID card or Hong Kong and Macau pass

- Click “Add Bank Card” in the wallet

- Bind your Hong Kong card (HSBC Blue Lion Card / ZA Card / Ant Bank Card, etc.)

- After completion, select “Hong Kong Wallet” when scanning the QR code to pay in the Mainland.

Alternative: AlipayHK

- Download AlipayHK App

- Register with Hong Kong mobile phone number + identity verification

- Bind Hong Kong Card

- Support urban public transportation in the Greater Bay Area (subway buses in Shenzhen, Guangzhou, etc.)

Comparison of costs for each plan

Things to note

- HSBC Red Lion Card (UnionPay) cannot be bound to WeChat/Alipay, you must apply for Blue Lion Card (MasterCard)

- HSBC’s default third-party payment limit may be 0, and you need to manually increase the limit in online banking

- ZA Card (Visa debit card) can be bound directly, which is more convenient

- WeChat Pay HK requires intermediate or above certification to make large purchases (basic annual limit HKD 100,000)

Withdraw money from PayPal to HSBC Hong Kong (personal test to get the money)

To add a scenario that programmers/independent developers are concerned about: I have some overseas SaaS income sitting in PayPal, and there has never been a good way to withdraw it. I tried it after opening an HSBC account – the money arrived, there was no handling fee, only the PayPal exchange rate depreciation.

Operation process

1. Bind HSBC account to PayPal: PayPal → Wallet → Link Bank Account → Hong Kong SAR

Bank Code: 004

SWIFT:HSBCHKHHHKH

Branch code: first 3 digits of HSBC card number

Account number: last 9 digits of card number

1. Initiate a withdrawal: PayPal → Withdraw → Standard Transfer → Confirm the amount

3-6 working days to arrive

cost

The real cost is not the handling fee, but the PayPal exchange rate markup (about 2.5-3%). PayPal will force the conversion of USD to HKD, which cannot be avoided even if HSBC supports multi-currency accounts. For small overseas income, this loss is acceptable.

Things to note

- The PayPal name must be exactly the same as the bank account name (in capital pinyin)

- Don’t withdraw your balance all at once, leave 10-15% in case of refunds/disputes

- Proof of source of income may be required for amounts over USD 5,000

- For large withdrawals, consider using channels such as Wise or Payoneer for better rates.

Summary of trampling on pitfalls (tearfully compiled)

🔴 Pitfalls that must be avoided

🟢 Worry-saving tips

- After arriving in Hong Kong, first connect to the hotel WiFi before starting the operation. The network is stable.

- Open the virtual bank first (fast, 5 minutes), then open HSBC (a little longer)

- The purpose of opening an account is unified as “personal asset allocation”, it is simple and error-free

- Bring a power bank and open several apps continuously, which consumes a lot of power.

- If possible, bring two mobile phones (main phone + Android backup)

- Use the input method to record commonly used information in advance: ID number, mobile phone number, mainland address (pinyin version), email, etc. When opening an account, it will be automatically filled in with one click, saving you from having to type it over and over by hand – if you open four or five apps in a row, you have to fill in the same information several times. This method can save a lot of time.

What’s the cheapest way to transfer money across the border from Mainland China to Hong Kong?

Conclusion: To transfer money to BOCHK, use “BOC Express” and to transfer money to HSBC, use “HB World Life”. Both lines can achieve zero fees.

List of fees for each bank

TL;DR

Four steps to complete:

- Before departure — download the app + export entry record PDF + start roaming

- Arrive in Hong Kong — Connect to WiFi → Open App → Upload ID → Scan face → Fill in information

- Before leaving Hong Kong – Set up mobile banking (if you don’t do it, it will be in vain)

source

author:Lu Liqing_JimmyLv 2𐃏26

Release time: February 25, 2026 15:38

source:Original post link

Editorial Comment

The era of standing in a humid queue on Des Voeux Road Central just to get a basic savings account is effectively over. Jimmy Lv’s recent field report from early 2026 highlights a significant shift in the Hong Kong banking landscape: the "Information Gap" has moved from knowing which branch is "easy" to knowing which PDF timestamp the algorithm demands.

The core of this modern workflow is the "Entry/Exit Record" PDF. In previous years, a simple stamp in a passport or a landing slip sufficed. Now, the digital KYC (Know Your Customer) process has become hyper-specific. The requirement for a "same-day" generated PDF from the National Immigration Administration is the ultimate gatekeeper. It’s a clever, if frustrating, way for banks to ensure the applicant is currently in the territory without requiring a human teller to verify a physical document. If you generate that PDF at 11:55 PM and apply at 12:05 AM, you’ve already lost. This is the kind of granular technical detail that separates a successful "one-hour" run from a wasted trip.

The failure of Bank of China (BOC) HK in this report is also telling. Despite being the most "mainland-friendly" institution on paper, their legacy app infrastructure often struggles with modern hardware—specifically the focal lengths of newer smartphone cameras (like the iPhone 16/17 series) and high-traffic Wi-Fi environments. It serves as a reminder that in the race to digitize, the "Big Four" traditional banks are often outpaced by virtual challengers like ZA Bank or Ant Bank. For a tech-savvy user, these virtual banks aren't just "alternatives"; they are the primary infrastructure for moving money into the global ecosystem.

From a senior editor's perspective, the most valuable part of this guide isn't the "how-to" of opening the account, but the "how-to" of keeping it. We are seeing a massive uptick in "zombie accounts"—accounts opened by mainland visitors that are frozen six months later due to inactivity or suspicious "round-tripping" (moving money in and immediately out). The advice to bind these cards to WeChat Pay HK is the real "pro tip." It solves a dual problem: it keeps the account active through small, legitimate domestic transactions in the mainland, and it bypasses the $50,000 annual forex quota by utilizing the Hong Kong wallet’s settlement system.

However, we must address the "why." Why go through this? For developers and independent creators, the PayPal-to-HSBC pipeline remains one of the few ways to receive overseas SaaS revenue without losing a massive percentage to predatory middleman fees or getting stuck in the "source of funds" bureaucracy of mainland banks.

The bottom line: Hong Kong banking has become an "app-first" game. If you have a stable Wi-Fi connection, a modern smartphone with NFC, and the discipline to follow a 33-step checklist without skipping the "initialization" phase, you can build a global financial bridge in the time it takes to finish a dim sum lunch. Just don’t expect the legacy giants like BOC to make it easy for you; the future of HK banking clearly belongs to the institutions that have figured out how to make their apps work as well as their vaults.