Editor’s Brief

The cross-border digital finance boom has created a dangerous "gold rush" mentality where users trade sensitive biometric data for access to overseas banking and eSIM services. This report highlights the irreversible risks of handing over passports and facial scans to unverified niche platforms, which can lead to permanent exclusion from the global financial system and lifelong identity theft.

Key Takeaways

- Biometric Permanence:** Unlike passwords, leaked facial data and passport scans cannot be reset. Once harvested by shady platforms, this data becomes a permanent asset for deepfake fraud and identity synthesis.

- The Global Blacklist:** Minor compliance triggers on low-tier Fintech platforms can propagate through AML (Anti-Money Laundering) networks, potentially leading to "de-risking" by major institutions like the FDIC or European banks.

- The "Information Gap" Trap:** Many "shortcuts" shared in social media circles are actually funnels for data harvesting. Niche eSIM providers and offshore banks often lack the security infrastructure to protect the data they demand.

- Digital Sovereignty via e-Residency:** Programs like Estonia’s e-Residency offer a legitimate "firewall" for privacy, allowing users to conduct business and banking with a digital ID rather than exposing their primary physical documents to every service provider.

Introduction

In the craze of cross-border overseas travel, many novices blindly hand over passports and facial information to various niche platforms in order to open overseas banks or eSIM. Blogger Ni Fulei reminded by reviewing recent cases that this “register first and then talk” mentality can easily lead to identity fraud or even being included in a compliance blacklist. In the digital age, the leakage of biological information is often irreversible. Carefully identifying the underlying background of the platform is the first lesson in cross-border security.

focus

- Be wary of KYC audits on niche FinTech platforms. Once passport and face data are leaked, they may be used for illegal activities, resulting in individuals being permanently blacklisted from the global banking system.

- Recognize the uniqueness of biometric information, and passwords can be changed if they are leaked. However, once identity documents and facial data are illegally stored or sold, they will face lifelong digital security threats.

- Be careful when using virtual accounts or eSIMs from unknown sources. Such tools can easily trigger the risk control of major manufacturers, leading to account closure or credit damage. It is recommended to give priority to mainstream compliance service providers.

Remark

Many times, the “information gap” we pursue is actually a hole dug by others. Tools in the cross-border circle are updated very quickly, but the underlying logic always puts compliance first. Instead of struggling to prove your innocence after an accident, it is better to spend an extra five minutes memorizing the evidence before registering. Remember, your digital identity is your most core asset. Don’t lose your ticket to the global financial market just to save the registration fee.

Editorial comments

This article “X Import: Nifulei’s Breakthrough – [Warning!] A must-read for cross-border novices: Overseas banks, eSIM, and digital identity comprehensive privacy protection guide. Don’t “sell” your privacy yourself” comes from the X social platform, and the author is Nifulei’s Breakthrough. Judging from the completeness of the content, the density of key information given in the original text is relatively high, especially in the core conclusions and action suggestions, which are highly implementable. Recently, many newcomers have sent private messages to Nifulei to ask whether some “new software” is reliable and whether they have heard of it. When I see the “XXX Opening Guide” shared by other self-media bloggers or WeChat group friends, I rush to upload sensitive information such as passport, ID card, mobile phone number, and even facial recognition to register an account. Although the steps are simple, they may lead to long-term risks in the future. To be honest, Ni Fulei himself does not fully understand the underlying situation of some so-called “new software”. When doing any product strategy, I will spend a certain amount of time on the basis of investigating as comprehensively as possible… For readers, its most direct value is not “knowing a new point of view”, but being able to quickly see the conditions, boundaries and potential costs behind the point of view. If this content is broken down into verifiable judgments, it would at least include the following aspects: Recently, many newcomers have sent private messages to Nifulei to ask whether some “new software” is reliable and whether they have heard of it. I saw “XXX activation…” shared by other self-media bloggers or WeChat group friends; although the steps are simple, they may lay long-term hidden dangers for the future. Among these judgments, the conclusion part is often the easiest to disseminate, but what really determines the practicality is whether the premise assumptions are established, whether the sample is sufficient, and whether the time window matches. We recommend that readers, when quoting this type of information, first check the data source, release time and whether there are platform environment differences, to avoid mistaking “scenario-based experience” for “universal rules.” From the perspective of industry impact, this type of content usually has a short-term guiding effect on product strategy, operational rhythm and resource investment, especially in topics such as AI, development tools, growth and commercialization. From an editorial perspective, we are more concerned about “whether it can withstand subsequent fact testing”: first, whether the results can be reproduced, secondly, whether the method can be transferred, and thirdly, whether the cost is affordable. The source is x.com, and readers are recommended to use it as one of the inputs for decision-making, rather than the only basis. Finally, a practical suggestion: If you are ready to act on this, you can conduct small-scale verification first, and then gradually expand investment based on feedback; if the original article involves revenue, policy, compliance, or platform rules, please refer to the latest official announcement and retain the rollback plan. The significance of reprinting is to improve the efficiency of information circulation, but the value of content is truly formed in secondary judgment and localization practice. Based on this principle, the editorial comments accompanying this article will continue to emphasize verifiability, boundary awareness, and risk control to help you turn “visible information” into “implementable knowledge.”

Recently, many newcomers have sent private messages to Nifulei to ask whether some “new software” is reliable and whether they have heard of it. When I see the “XXX Opening Guide” shared by other self-media bloggers or WeChat group friends, I rush to upload sensitive information such as passport, ID card, mobile phone number, and even facial recognition to register an account.

Although the steps are simple, they may lead to long-term risks in the future.

To be honest, Ni Fulei himself does not fully understand the underlying situation of some so-called “new software”. When I do any product strategy, I will spend a certain amount of time, based on as comprehensive an investigation as possible, combined with my own knowledge system, filtering visible risks, and then sorting out useful strategy content. But even so, there may still be vulnerabilities and unknown risks that I cannot predict in advance.

Core question: Is your private data really safe?

In the digital age, a scan of a passport or a photo of a face can be copied, disseminated, and even used in unexpected scenarios. Don’t think that “it’s just testing the waters without saving money”, the risks often start from here.

Below, Nifulei dismantles these hidden dangers step by step and provides practical suggestions.

At the same time, don’t forget to follow my YouTube channel “The Story of Mud Thunder”, so that you can view the complete tutorials at any time, unlock more exciting content, and get the latest practical strategies as soon as possible.

1. Risks of misuse of private information:

The risk of misuse of privacy is far greater than you think. Many people have the mentality of “register first and then talk”, but the reality is: once your identity data is uploaded, it is equivalent to handing the key to a stranger.

The following are common risks, based on global financial regulatory reports and real case summaries:

1. Identity is used as a “black account” or money laundering tool

Non-compliant platforms (especially emerging FinTech or niche exchanges) often use user data to create fake accounts for third parties.

The 2023 EU Anti-Money Laundering Report shows that more than 30% of cross-border money laundering cases involve identity theft. Once the platform is investigated, your passport number may be listed as a “person involved”, resulting in bank freezing or legal investigation. Even if you are innocent, it will take months to prove your innocence.

1. “Zero Tolerance” for Overseas Bank Compliance: The Consequences Will Have Lifelong Impact

Regulatory frameworks such as the US FDIC and EU MiFID II have extremely strict KYC requirements. Registering with a fake identity or a low-quality platform may trigger:

- Permanent blacklist: If you are flagged by OFAC (Office of Foreign Assets Control of the U.S. Department of the Treasury), it will be even more difficult to open a subsequent account.

– Cross-border restrictions: affecting FATCA (Foreign Account Tax Compliance Act) reporting and indirectly affecting visa applications.

Real case: In 2024, a Chinese user was blocked from the U.S. banking system due to a data leak from a small European bank, and has been unable to invest in U.S. stocks normally.

1. The trap of “never deleting” face and ID data

Many platforms claim to be “for verification only,” but privacy policies often allow for data sharing or long-term storage. Although GDPR (EU General Data Protection Regulation) has a right of withdrawal, cross-border enforcement is difficult – your data may have flowed to a third-party server.

According to the latest statistics in 2025, biometric information accounts for 25% of global data breaches, and is often used in deepfake fraud.

1. The “invisible bomb” of eSIM/virtual account

Unofficial eSIMs (such as virtual numbers provided by some gray apps) are easily identified as “high risk” by the platform’s risk control system.

Result: WhatsApp accounts were repeatedly verified, Google services were restricted, and credit scores were even accumulated, affecting the use of real SIM cards. Although popular eSIM providers such as Airalo or Nomad are reliable, if the source is unknown, the account suspension rate is as high as 40% (based on user feedback community data).

2. Core principles:

Why is “True ID” not a panacea? To put it simply: your passport, face and mobile phone number are lifelong digital assets, not free “registration coupons”.

- Avoid it if you can: give priority to using virtual tools to test requirements.

- If you’re not sure, avoid it: The data leakage rate of niche platforms is 3-5 times that of mainstream platforms.

– Leakage is permanent: Unlike passwords that can be changed, once biometric data is leaked, it is irreversible.

Remember: Compliance platforms welcome prudent users, and eagerness for success is often a trap.

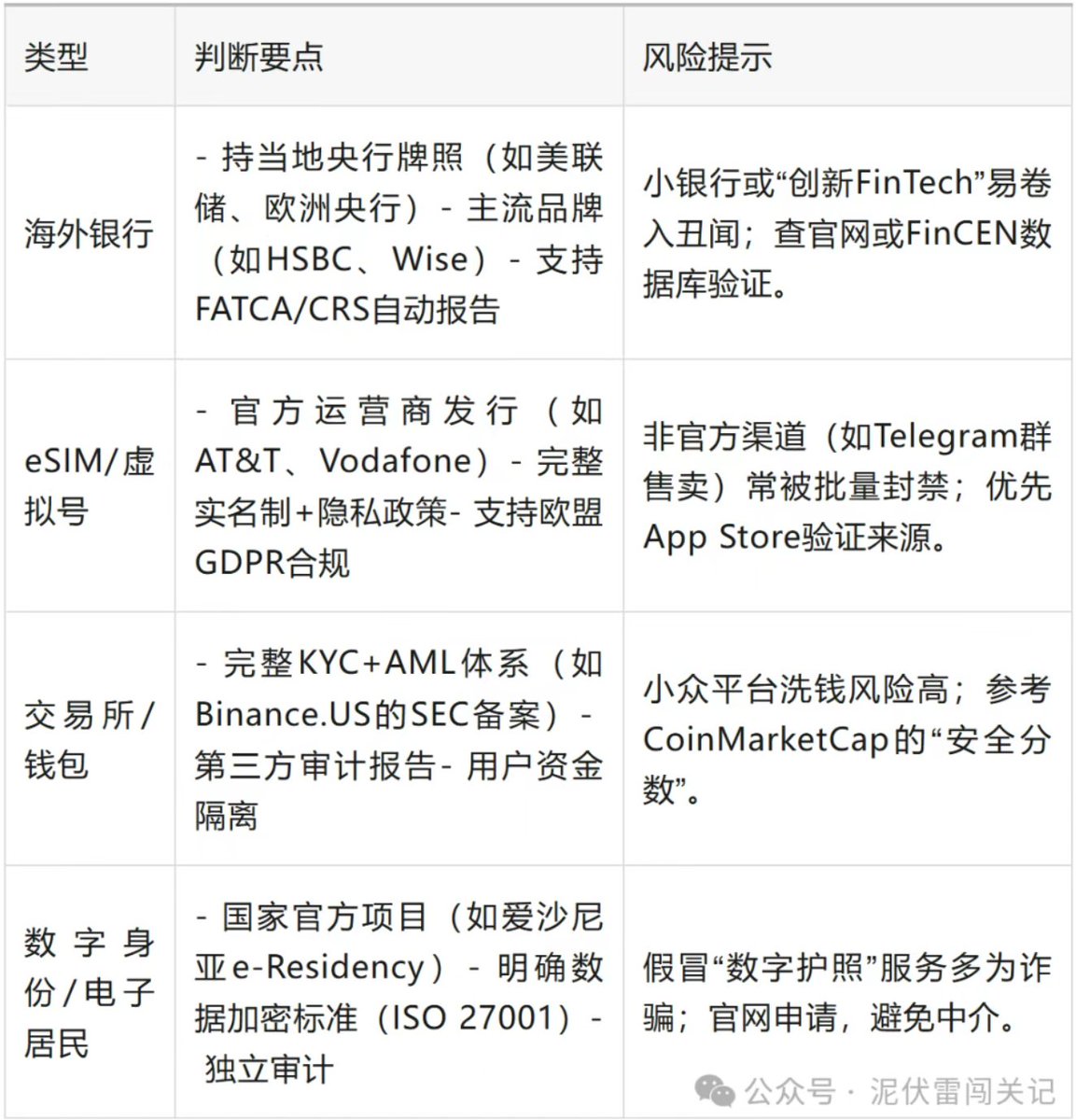

3. How to identify platforms:

Don’t be fooled by “looks reliable”. Before registering, take 5 minutes to check yourself and avoid 80% of pitfalls.

The following is an expanded judgment framework, incorporating global regulatory standards:

Tips: Use tools such as Who.is to check the domain name registration time (>5 years is more reliable), or search for “platform name + complaints” to see Reddit/Trustpilot feedback.

4. Actual protection:

From assessment to implementation, one-stop guide to privacy protection is not “remediation after the fact” but “design beforehand”. Here’s the step-by-step guide:

1. Needs assessment: Don’t pay for “maybe”

Ask yourself first: Is this overseas collection? Invest in US stocks? Or international payment?

- Low requirement: Test with a simulator (such as Paper Trading App).

– Medium demand: Start with a small amount and monitor for a limited time.

According to a 2025 World Bank report, 70% of cross-border users “regret” opening unnecessary accounts – make a list first and then act.

- Embracing digital identity: The best option for walls

- Estonian e-Residency: an official EU project that provides digital ID cards and supports remote registration of companies/banks. Advantages: Data is encrypted locally and is not bound to a real passport.

– Other options: Portugal Golden Visa Digital Edition, UAE Virtual Residency Program, or third parties such as Civic Wallet (blockchain identity).

Usage tips: Use it only for “secondary accounts”, leaving the main identity for high-value operations. The cost is about 100-200 euros per year, which is worth the price.

🔍Recommended reading: The ultimate guide to digital citizenship and e-residents in 13 countries around the world | Full analysis of registration and application in Estonia, Palau, and Honduras. Preview

1. “Zero tolerance” for high-risk platforms

Be wary of: small Caribbean country banks (vulnerable to sanctions), emerging DEX exchanges, unofficial eSIMs (such as some VPN bundled services), unknown DeFi wallets.

Red flags: No privacy policy, forced facial recognition, multi-level proxy registration.

- Hierarchical privacy management: manage data like money

- Email/mobile phone number: Use ProtonMail (encrypted) + Google Voice (virtual account) to separate the platforms.

- Password: LastPass or 1Password generates a unique key to avoid the “123456” minefield.

- Policy check: Read the privacy policy and make sure “data is not sold or shared.”

5. Digital electronic resident certificate:

A Tool, Not a Panacea Tools such as e-Residency are privacy “shields”, but don’t myth them. Based on official documentation, taking Estonia as an example:

✅What you can do (high practical value):

- As a legal digital ID, register an EU company and bank account.

- Isolated privacy: operate with e-ID without exposing real passport/face.

- Support cross-border payments: Integrate SEPA transfers and receive payments without borders.

- Extension: Added NFT Art/Telemedicine Certification in 2025.

⛔What it can’t do (don’t expect it to be a cure-all):

- Not replacing tax residents: still need to declare global income (under the CRS framework).

- Not exempt from compliance: Platforms may still require additional verification.

- Unlimited is not guaranteed: If you open a US stock account, an additional SSN may be required.

- Limitations: Not applicable to immigration/visas, digital domain only.

In short: it is a “firewall”. When used correctly, it can block 99% of leaks; when used incorrectly, it becomes an additional burden.

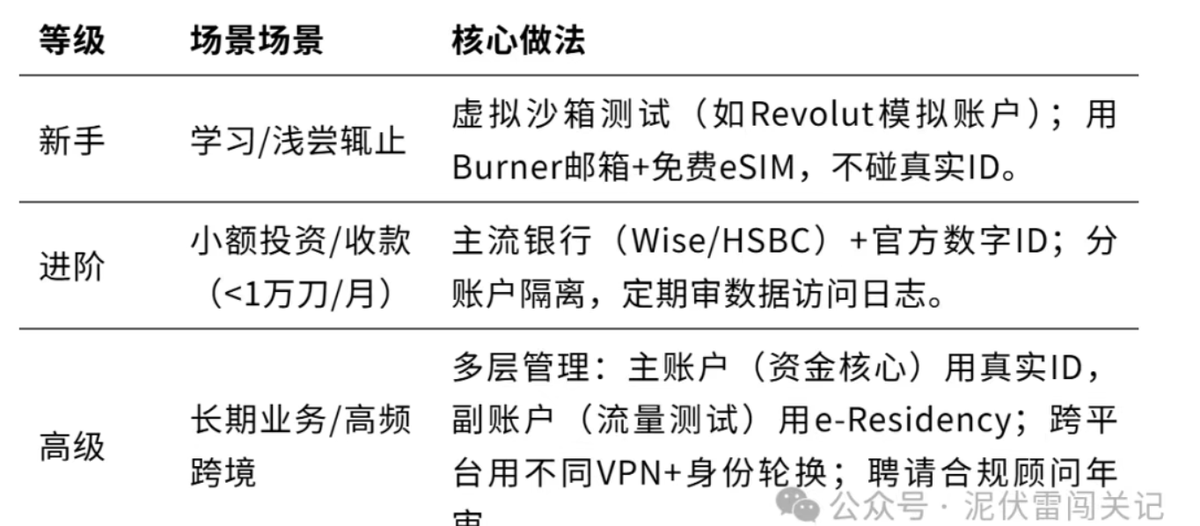

6. Cross-border privacy protection plan for novices:

The graded advanced path is based on your “firepower level”, choose the right path to avoid pitfalls:

Ni Fulei’s “sincere” advice:

🫨Slow down and you will go further. There are also many “good-hearted people” who “seed” people across the “border” world. But your passport, facial data, and mobile phone number are not “trophies” to show off, but a fortress to protect you for a lifetime.

The pleasure of following the trend of registration is fleeting; the habit of safety and compliance can stay with you for ten years.

From today on: ask more “is it worth it” and “is it necessary” and less “just in case”. In the financial jungle, speed won’t kill you, only recklessness will. It’s difficult at first, but once you develop it, freedom will follow you.

Finally, forward it to important friends around you.

If you are a newbie going overseas, it is recommended to check out the newcomer guide below and open these platforms~

🛠Click to get: →❤ Navigation Guide for Newcomers ❤←

source

author:A story about mud and thunder

Release time: January 23, 2026 09:49

source:Original post link

Editorial Comment

The current obsession with "going global" has blinded many to the predatory nature of the digital identity market. As a senior editor who has watched the evolution of Fintech from its early "disruptive" days to its current state of hyper-regulation, I find the trend of "blind registration" particularly alarming. We are seeing a massive asymmetry between the perceived value of an overseas account and the actual cost of the data being traded to acquire it.

The core of the issue is that most newcomers view a passport scan or a "liveness check" as a mere administrative hurdle—a digital ticket to be punched. In reality, you are handing over the keys to your financial future. In the legacy banking world, if a local branch leaked your data, the damage was often contained by geography or jurisdiction. In the modern, interconnected KYC (Know Your Customer) ecosystem, a data breach at a fly-by-night "Neo-bank" in a loosely regulated jurisdiction can have a ripple effect that hits your credit score or your ability to open a brokerage account in New York or London years later.

We need to talk about the "Blacklist" effect. Global finance is increasingly governed by automated risk-scoring algorithms. If your identity is flagged—even erroneously—because it was used by a third party who bought your leaked data to wash funds, "proving your innocence" is a Herculean task. There is no central "Help Desk" for global financial compliance. Once you are marked as high-risk by an AML engine, you are effectively ghosted by the system.

The source text mentions the "five-minute background check," and I cannot stress this enough. If you are using a platform that hasn't existed for at least five years, or one that lacks a clear, enforceable privacy policy under a reputable jurisdiction like the GDPR, you are the product, not the customer. The "information gap" that many influencers sell is often just a lack of due diligence. They profit from the referral; you bear the lifetime risk of the data leak.

For those serious about cross-border operations, the shift must be from "convenience" to "compliance." This means adopting a tiered approach to privacy. Use encrypted mail services like Proton for all financial communications. Use virtual numbers for initial testing. Most importantly, leverage official digital identity programs like Estonia’s e-Residency or similar "digital nomad" IDs. These programs act as a sophisticated buffer. They provide a government-backed digital identity that is recognized by major banks but keeps your primary physical passport out of the hands of every minor app developer.

The "X Import" story is a necessary cold shower for the community. The digital frontier is not a playground; it is a high-stakes environment where your identity is the most valuable currency you own. If a service is free or "too easy" to join, ask yourself why they want your face so badly. In the financial jungle, speed is often a liability, and caution is the only real hedge against obsolescence. Don't trade a lifetime of financial mobility for a temporary "shortcut" that leads to a dead end.